Dividend Stocks

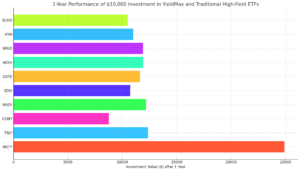

YieldMax ETFs and Alternatives: Chasing High Yields in 2025 — Risks, Rewards, and Alternatives

May 7, 2025

The Market is down and yields are up. A lot…

Read More

SCHD: Should You Buy Schwab US Dividend Equity ETF?

July 8, 2024

If you’re looking for a high-quality dividend ETF then there’s…

Read More

Will ZIM Relaunch its Dividend Soon?

May 6, 2024

ZIM Integrated Shipping Services (NYSE: ZIM) is set to release…

Read More

Best 25 Blue Chip Stocks List for a Recession

October 4, 2022

This list of blue chip stocks can help investors through the recession. These companies continue to pay dividends.

25 High-Yield Dividend Stocks

September 29, 2022

The extra income from high-yield dividend stocks can help during a downturn. Here are some of the highest-yielding stocks to buy.

6 Best Stocks to Buy Right Now

September 28, 2022

The best stocks to buy right now are well below their highs. When the market rebounds, these stocks should move higher.

6 Dividend Stocks to Buy in September

September 15, 2022

The market is handing us better buying opportunities. Here are the best dividend stocks to buy this month for extra income.

6 Best High-Yield Dividend Stocks

September 8, 2022

As the market goes through a downturn, these high-yield dividend stocks can help weather the storm with extra income.

- 1

- 2

- 3

- …

- 20

- Next Page »